Analyzing and Predicting Financial Time Series Data Using Recurrent Neural Networks

DOI:

https://doi.org/10.5281/zenodo.12786717ARK:

https://n2t.net/ark:/40704/JIEAS.v2n4a03References:

24Keywords:

Financial Time Series Prediction, Recurrent Neural Networks, Long Short-Term Memory Networks, LSTM, Time Series Analysis, Deep Learning, ARIMA, GARCH, Stock Price Prediction, Exchange Rate Forecasting, Volatility Modeling, Machine Learning in Finance, Data Preprocessing, Hyperparameter Tuning, Prediction Accuracy, Financial Forecasting, Sequential Data Modeling, Bidirectional LSTM, Technical indicatorsAbstract

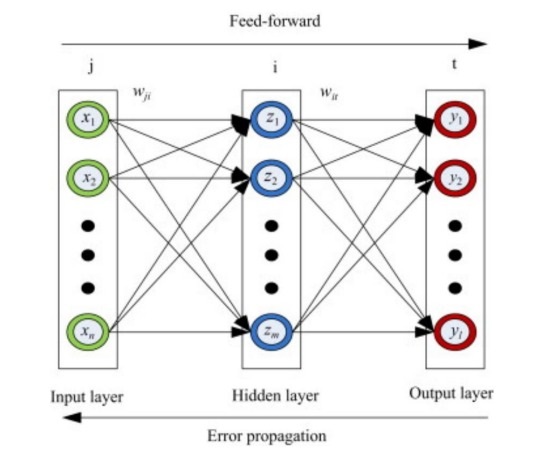

Financial time series data, characterized by its inherent complexity and volatility, presents significant challenges for accurate prediction. Traditional statistical models often fall short in capturing the intricate patterns and dependencies within the data. Recurrent Neural Networks (RNNs), particularly Long Short-Term Memory (LSTM) networks, offer a promising solution by leveraging their ability to learn temporal dependencies and complex sequences. This paper explores the application of RNNs in analyzing and predicting financial time series data, examining their effectiveness, implementation challenges, and potential benefits. Specifically, we investigate the architecture of RNNs, the role of LSTM in mitigating issues such as the vanishing gradient problem, and the impact of hyperparameter tuning on model performance. Comprehensive experiments demonstrate the superiority of RNNs over traditional models, highlighting their potential to transform financial forecasting by improving prediction accuracy, adapting to dynamic market conditions, and reducing the need for extensive feature engineering.

Downloads

References

Box, G. E. P., Jenkins, G. M., & Reinsel, G. C. (2015). Time Series Analysis: Forecasting and Control. Wiley.

Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

Engle, R. F. (1982). Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica, 50(4), 987-1007.

Cao, L. J., & Tay, F. E. H. (2001). Financial forecasting using support vector machines. Neural Computing & Applications, 10(2), 184-192.

Fischer, T., & Krauss, C. (2018). Deep learning with long short-term memory networks for financial market predictions. European Journal of Operational Research, 270(2), 654-669.

Nelson, D. M., Pereira, A. C., & de Oliveira, R. A. (2017). Stock market's price movement prediction with LSTM neural networks. Proceedings of the International Joint Conference on Neural Networks (IJCNN), 1419-1426.

Liu, T., Cai, Q., Xu, C., Zhou, Z., Ni, F., Qiao, Y., & Yang, T. (2024). Rumor Detection with a novel graph neural network approach. arXiv Preprint arXiv:2403. 16206.

Liu, T., Cai, Q., Xu, C., Zhou, Z., Xiong, J., Qiao, Y., & Yang, T. (2024). Image Captioning in news report scenario. arXiv Preprint arXiv:2403. 16209.

Xu, C., Qiao, Y., Zhou, Z., Ni, F., & Xiong, J. (2024a). Accelerating Semi-Asynchronous Federated Learning. arXiv Preprint arXiv:2402. 10991.

Zhou, J., Liang, Z., Fang, Y., & Zhou, Z. (2024). Exploring Public Response to ChatGPT with Sentiment Analysis and Knowledge Mapping. IEEE Access.

Zhou, Z., Xu, C., Qiao, Y., Xiong, J., & Yu, J. (2024). Enhancing Equipment Health Prediction with Enhanced SMOTE-KNN. Journal of Industrial Engineering and Applied Science, 2(2), 13–20.

Zhou, Z., Xu, C., Qiao, Y., Ni, F., & Xiong, J. (2024). An Analysis of the Application of Machine Learning in Network Security. Journal of Industrial Engineering and Applied Science, 2(2), 5–12.

Zhou, Z. (2024). ADVANCES IN ARTIFICIAL INTELLIGENCE-DRIVEN COMPUTER VISION: COMPARISON AND ANALYSIS OF SEVERAL VISUALIZATION TOOLS.

Xu, C., Qiao, Y., Zhou, Z., Ni, F., & Xiong, J. (2024b). Enhancing Convergence in Federated Learning: A Contribution-Aware Asynchronous Approach. Computer Life, 12(1), 1–4.

Wang, L., Xiao, W., & Ye, S. (2019). Dynamic Multi-label Learning with Multiple New Labels. Image and Graphics: 10th International Conference, ICIG 2019, Beijing, China, August 23--25, 2019, Proceedings, Part III 10, 421–431. Springer.

Wang, L., Fang, W., & Du, Y. (2024). Load Balancing Strategies in Heterogeneous Environments. Journal of Computer Technology and Applied Mathematics, 1(2), 10–18.

Wang, L. (2024). Low-Latency, High-Throughput Load Balancing Algorithms. Journal of Computer Technology and Applied Mathematics, 1(2), 1–9.

Wang, L. (2024). Network Load Balancing Strategies and Their Implications for Business Continuity. Academic Journal of Sociology and Management, 2(4), 8–13.

Li, W. (2024). The Impact of Apple’s Digital Design on Its Success: An Analysis of Interaction and Interface Design. Academic Journal of Sociology and Management, 2(4), 14–19.

Wu, R., Zhang, T., & Xu, F. (2024). Cross-Market Arbitrage Strategies Based on Deep Learning. Academic Journal of Sociology and Management, 2(4), 20–26.

Wu, R. (2024). Leveraging Deep Learning Techniques in High-Frequency Trading: Computational Opportunities and Mathematical Challenges. Academic Journal of Sociology and Management, 2(4), 27–34.

Wang, L. (2024). The Impact of Network Load Balancing on Organizational Efficiency and Managerial Decision-Making in Digital Enterprises. Academic Journal of Sociology and Management, 2(4), 41–48.

Chen, Q., & Wang, L. (2024). Social Response and Management of Cybersecurity Incidents. Academic Journal of Sociology and Management, 2(4), 49–56.

Song, C. (2024). Optimizing Management Strategies for Enhanced Performance and Energy Efficiency in Modern Computing Systems. Academic Journal of Sociology and Management, 2(4), 57–64.

Downloads

Published

How to Cite

Issue

Section

ARK

License

Copyright (c) 2024 The author retains copyright and grants the journal the right of first publication.

This work is licensed under a Creative Commons Attribution 4.0 International License.