Anomaly Pattern Detection in High-Frequency Trading Using Graph Neural Networks

DOI:

https://doi.org/10.70393/6a69656173.323430ARK:

https://n2t.net/ark:/40704/JIEAS.v2n6a09Disciplines:

Artificial Intelligence TechnologySubjects:

Machine LearningReferences:

20Keywords:

Graph Neural Networks, High-Frequency Trading, Market Manipulation Detection, Financial Market SurveillanceAbstract

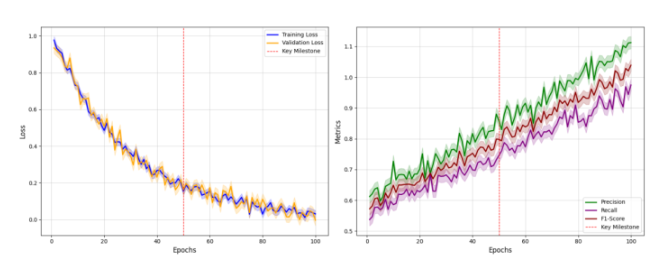

This paper presents a new method for detecting abnormal patterns in high-frequency trading (HFT) using graph neural networks (GNNs). The increasing sophistication of trading algorithms and the large volume of data have often created unprecedented challenges for traditional market analysis. Our framework addresses these challenges by introducing a GNN-based architecture that takes advantage of the physical and structural properties of business data. The proposed method transforms HFT data into graphical models where the nodes represent market conditions and the edges capture their physical and price relationships. A specialized GNN architecture, incorporating attention mechanisms and temporal convolution modules, is developed to learn complex trading patterns and identify potential anomalies. The model is evaluated on high-frequency trading data from five major stocks listed on NASDAQ, spanning six months of trading activity with over 10 million events. Experimental results demonstrate superior performance compared to existing approaches, achieving a 15% improvement in detection accuracy and maintaining robust performance across different market conditions. The framework exhibits particular strength in identifying complex manipulation patterns while maintaining low false positive rates. Our approach processes large volumes of trading data in real time with significantly reduced computational requirements compared to traditional methods. This research contributes to the development of more effective market surveillance systems and provides valuable insights for regulatory authorities in maintaining market integrity.

Downloads

References

Zhou, J., Wang, S., & Ou, Y. (2024, June). Fourier Graph Convolution Transformer for Financial Multivariate Time Series Forecasting. In 2024 International Joint Conference on Neural Networks (IJCNN) (pp. 1-8). IEEE.

Yadav, S., Singh, A., Singh, S. K., Singh, V. P., Vuyyuru, V. A., & Balakumar, A. (2024, June). Improving Market Efficiency and Profitability in High-Frequency Trading Using Neural Network-Based Deep Learning Techniques. In 2024 15th International Conference on Computing Communication and Networking Technologies (ICCCNT) (pp. 1-6). IEEE.

Yuan, Z., Liu, J., Zhou, H., Zhang, D., Liu, H., Zhu, N., & Xiong, H. (2023). LEVER: Online Adaptive Sequence Learning Framework for High-Frequency Trading. IEEE Transactions on Knowledge and Data Engineering.

Xu, H., Zhang, Y., & Xu, Y. (2023). Promoting Financial Market Development-Financial Stock Classification Using Graph Convolutional Neural Networks. IEEE Access, 11, 49289-49299.

Safa, K., Belatreche, A., & Ouadfel, S. (2024, June). Stock Price Manipulation Detection using Variational Autoencoder and Recurrence Plots. In 2024 International Joint Conference on Neural Networks (IJCNN) (pp. 1-8). IEEE.

Zheng, W., Yang, M., Huang, D., & Jin, M. (2024). A Deep Learning Approach for Optimizing Monoclonal Antibody Production Process Parameters. International Journal of Innovative Research in Computer Science & Technology, 12(6), 18-29.

Ma, X., Wang, J., Ni, X., & Shi, J. (2024). Machine Learning Approaches for Enhancing Customer Retention and Sales Forecasting in the Biopharmaceutical Industry: A Case Study. International Journal of Engineering and Management Research, 14(5), 58-75.

Cao, G., Zhang, Y., Lou, Q., & Wang, G. (2024). Optimization of High-Frequency Trading Strategies Using Deep Reinforcement Learning. Journal of Artificial Intelligence General Science (JAIGS) ISSN: 3006-4023, 6(1), 230-257.

Wang, G., Ni, X., Shen, Q., & Yang, M. (2024). Leveraging Large Language Models for Context-Aware Product Discovery in E-commerce Search Systems. Journal of Knowledge Learning and Science Technology ISSN: 2959-6386 (online), 3(4).

Li, H., Sun, J., & Ke, X. (2024). AI-Driven Optimization System for Large-Scale Kubernetes Clusters: Enhancing Cloud Infrastructure Availability, Security, and Disaster Recovery. Journal of Artificial Intelligence General Science (JAIGS) ISSN: 3006-4023, 2(1), 281-306.

Xia, S., Wei, M., Zhu, Y., & Pu, Y. (2024). AI-Driven Intelligent Financial Analysis: Enhancing Accuracy and Efficiency in Financial Decision-Making. Journal of Economic Theory and Business Management, 1(5), 1-11.

Zhang, H., Lu, T., Wang, J., & Li, L. (2024). Enhancing Facial Micro-Expression Recognition in Low-Light Conditions Using Attention-guided Deep Learning. Journal of Economic Theory and Business Management, 1(5), 12-22.

Wang, J., Lu, T., Li, L., & Huang, D. (2024). Enhancing Personalized Search with AI: A Hybrid Approach Integrating Deep Learning and Cloud Computing. International Journal of Innovative Research in Computer Science & Technology, 12(5), 127-138.

Ma, X., Zeyu, W., Ni, X., & Ping, G. (2024). Artificial intelligence-based inventory management for retail supply chain optimization: a case study of customer retention and revenue growth. Journal of Knowledge Learning and Science Technology ISSN: 2959-6386 (online), 3(4), 260-273.

Zheng, H.; Wu, J.; Song, R.; Guo, L.; Xu, Z. Predicting Financial Enterprise Stocks and Economic Data Trends Using Machine Learning Time Series Analysis. Applied and Computational Engineering 2024, 87, 26–32.

Ju, C., & Zhu, Y. (2024). Reinforcement Learning‐Based Model for Enterprise Financial Asset Risk Assessment and Intelligent Decision‐Making.

Huang, D., Yang, M., & Zheng, W. (2024). Integrating AI and Deep Learning for Efficient Drug Discovery and Target Identification.

Yang, M., Huang, D., & Zhan, X. (2024). Federated Learning for Privacy-Preserving Medical Data Sharing in Drug Development.

Li, L., Zhang, Y., Wang, J., & Ke, X. (2024). Deep Learning-Based Network Traffic Anomaly Detection: A Study in IoT Environments.

Li, H., Wang, G., Li, L., & Wang, J. (2024). Dynamic Resource Allocation and Energy Optimization in Cloud Data Centers Using Deep Reinforcement Learning. Journal of Artificial Intelligence General Science (JAIGS) ISSN: 3006-4023, 1(1), 230-258.

Downloads

Published

How to Cite

Issue

Section

ARK

License

Copyright (c) 2024 The author retains copyright and grants the journal the right of first publication.

This work is licensed under a Creative Commons Attribution 4.0 International License.