Development of AI Multi-Agent Frameworks for Financial Services

DOI:

https://doi.org/10.70393/6a69656173.333337ARK:

https://n2t.net/ark:/40704/JIEAS.v3n6a01Disciplines:

Artificial Intelligence TechnologySubjects:

Machine LearningReferences:

11Keywords:

Large Language Models (LLMs), Multi-agent Architectures, Financial Services, Hybrid Edge–cloud FrameworksAbstract

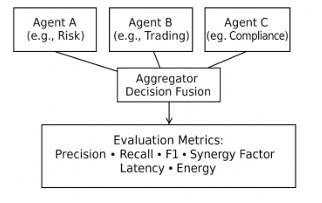

Large-language-model-based multi-agent architectures and distributed AI components are rapidly reshaping financial services. They enable autonomous decision-making, collaboration in problem-solving, and automation of complex workflows across risk management, trading, compliance, fraud detection, and customer interaction. However, existing frameworks face significant tensions between scalability, regulatory requirements, and real-time performance in highly dynamic markets. This paper revisits the current landscape of AI multi-agent frameworks for finance and proposes a refined perspective emphasizing framework architecture, quantitative evaluation, and governance. We briefly reference related developments in small-sample prompt-based classification and hybrid edge–cloud frameworks.

Downloads

References

[1] Qi, R., & Hu, L. (2025). Stock Price Prediction of Apple Inc. Based on LSTM Model: An Application of Artificial Intelligence in Individual Stock Analysis. European Journal of AI, Computing & Informatics, 1(3), 1-9.

[2] Hu, L., Wu, Q., & Qi, R. (2025). Empowering smart app development with SolidGPT: an edge–cloud hybrid AI agent framework. Advances in Engineering Innovation, 16(7), 86-92.

[3] Hu, L. (2025). Hybrid Edge-AI Framework for Intelligent Mobile Applications: Leveraging Large Language Models for On-device Contextual Assistance and Code-Aware Automation. Journal of Industrial Engineering and Applied Science, 3(3), 10-22.

[4] Hu, L. (2025). Topic Classification of Small Sample News Based on Prompt Engineering. Applied and Computational Engineering, 170, 101-107.

[5] Qi, R. (2025). Financial News Sentiment Analysis and Market Sentiment Prediction Based on Large Language Models. Journal of Computer, Signal, and System Research, 2(6), 22-31.

[6] Qi, R. (2025). An Empirical Study on Credit Risk Assessment Using Machine Learning: Evidence from the Kaggle Credit Card Fraud Detection Dataset. Journal of Computer, Signal, and System Research, 2(5), 48-64.

[7] Qi, R. (2025). Loan Default Prediction and Feature Importance Analysis Based on the XGBoost Model. European Journal of Business, Economics & Management, 1(2), 141-149.

[8] Joshi, S. (2025). Architectures and Challenges of AI Multi-Agent Frameworks for Financial Services. Current Journal of Applied Science and Technology, Vol. 44, Issue 6.

[9] Ante, L. (2024). Autonomous AI Agents in Decentralized Finance: Market Dynamics, Application Areas, and Theoretical Implications. Application Areas, and Theoretical Implications (December 14, 2024).

[10] Hettiarachchi, I. (2025). THE RISE OF GENERATIVE AI AGENTS IN FINANCE: OPERATIONAL DISRUPTION AND STRATEGIC EVOLUTION. International Journal of Engineering Technology Research & Management, 447.

[11] Agnihotram, G., Sarkar, J., Kasthuri, M., & Balasubramaniam, V. (2025). Agentic AI for Risk Assessment Controllers in BFSI: A Technical Framework for Autonomous Risk Mitigation. Journal of Banking and Financial Dynamics, 9(10), 1-8.

Downloads

Published

How to Cite

Issue

Section

ARK

License

Copyright (c) 2025 The author retains copyright and grants the journal the right of first publication.

This work is licensed under a Creative Commons Attribution 4.0 International License.